Stablecoins are on pace to process between $40 trillion and $46 trillion in raw on-chain transaction volume in 2026, surpassing the annual payment volume processed by Visa for the first time. The bulk of that flow didn’t move through Ethereum, where USDT was born. It moved through Tron.

The split between Ethereum’s ERC-20 and Tron’s TRC-20 standards isn’t ideological. It’s measurable, and it explains the market structure that emerged for any platform processing high-frequency international transactions.

The Macro Shift to Stablecoins

Correspondent banking relationships contracted significantly over the past decade, with the steepest losses in exactly the regions where digital commerce grew fastest. Southeast Asia, Latin America, and parts of Africa saw entire markets routing payments through multiple intermediary banks before reaching their destination — each adding a fee, a delay, and a compliance review.

For high-volume international operators, the math stopped working. A platform processing thousands of cross-border transactions per day cannot absorb 3–5 day settlement windows, card processing fees of 2–4%, and the operational overhead of maintaining banking relationships across dozens of jurisdictions.

Stablecoins removed the correspondent layer entirely. A USDT transfer doesn’t traverse SWIFT, doesn’t pass through a Tier 1 bank, and doesn’t require either party to maintain an account anywhere. The blockchain is the settlement layer. Dollar denomination provides price stability between initiation and settlement — the combination legacy systems failed to deliver at acceptable cost. In Vietnam, Thailand, Indonesia, and large parts of Latin America, USDT now functions as a synthetic dollar with infrastructure the actual dollar lacks. Even Visa itself launched USDC settlement in the U.S. in December 2025, signaling that legacy payment networks are integrating stablecoins rather than competing with them.

Digital entertainment platforms were among the first sectors to migrate at scale. Online gaming and wagering operators in particular adopted stablecoin rails aggressively between 2022 and 2025, with the largest international platforms now processing the majority of deposits and withdrawals through USDT casino deposit networks rather than card processors or bank wires. The drivers are the same ones reshaping remittance and B2B commerce: settlement finality in minutes, fees that don’t scale with transaction size, and the ability to operate across jurisdictions without a correspondent bank in each one.

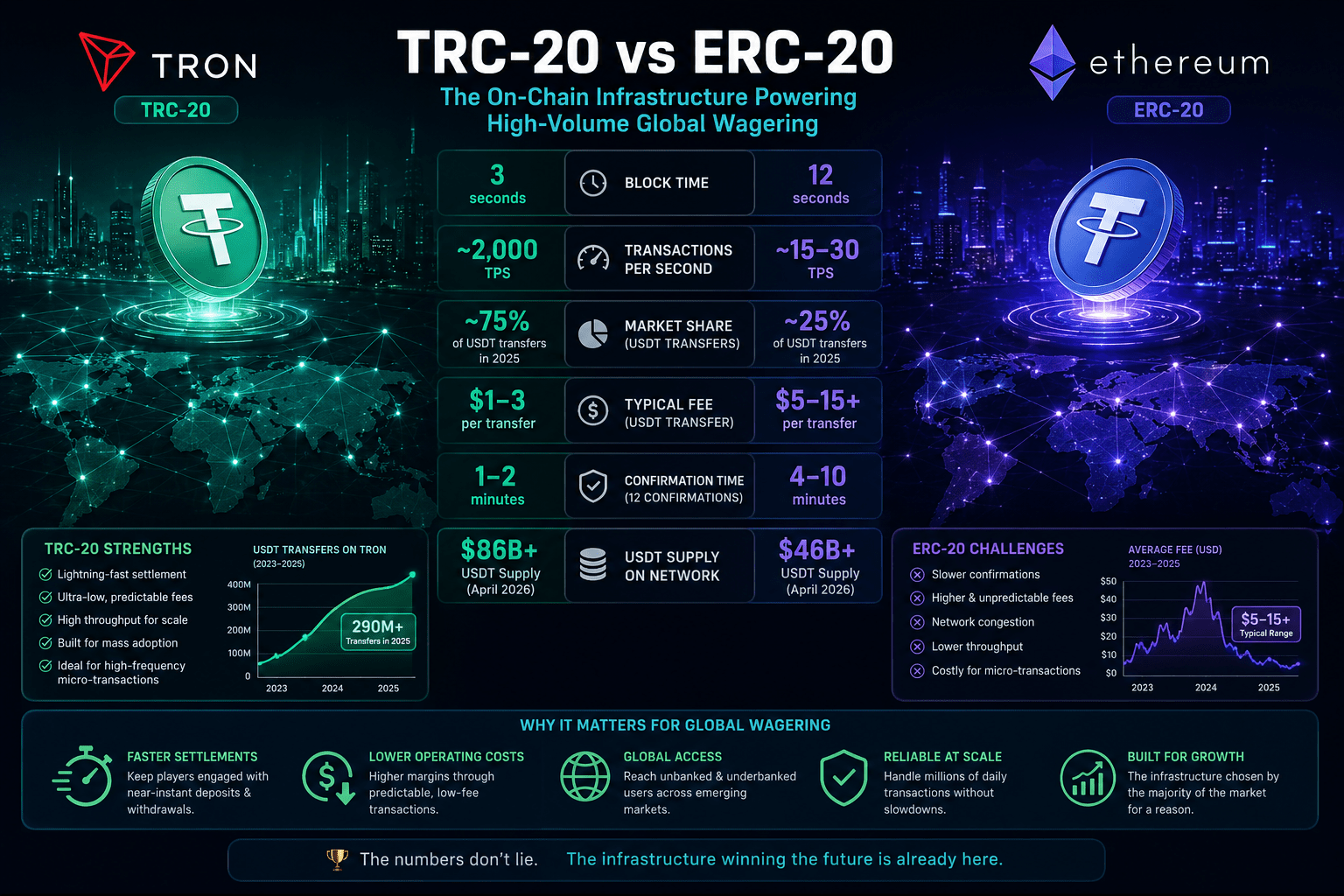

Network Congestion and Confirmation Speeds

Ethereum produces a block every 12 seconds and processes roughly 15–30 transactions per second at base layer. USDT transfers compete with DeFi activity, NFT mints, and L2 bridging traffic for that throughput. Tron is a delegated-proof-of-stake network that processes roughly 8 million transactions per day with block times of 3 seconds — and USDT accounts for the dominant share of that activity. Around 75% of all 2025 USDT transfer count happened on Tron, with over 290 million USDT transfers clearing on the network that year.

The supply distribution reflects where the actual flow lives. As of April 2026, Tron hosts about $86 billion of USDT, more than any other chain. In Q1 2026 alone, more than $7 billion of USDT left Ethereum — the largest quarterly drop on record — while Tron continued adding supply.

Under normal load, confirmation behavior diverges as follows:

| Confirmation stage | ERC-20 USDT | TRC-20 USDT |

| First inclusion in block | 15–45 seconds | 3–6 seconds |

| 12 confirmations (operator standard) | 2.5–4 minutes | 35–50 seconds |

| 20 confirmations | 4–10 minutes | 60–90 seconds |

Tron offers the fastest USDT transfers with confirmation times of 1–2 minutes, while Ethereum is slowest due to network congestion, typically 10–30 minutes during elevated activity. The UX implication is concrete: a user who sees “pending” for 35 seconds will wait. A user who sees “pending” for 12 minutes opens a support ticket, attempts a second deposit, or abandons the session — frequently all three. Operators that built their default rail on ERC-20 in 2018–2020 spent the early 2020s migrating to TRC-20 specifically to close this gap.

Transaction Costs and Economic Viability

The throughput differential matters. The fee differential is what decided the market.

Ethereum’s fee market is auction-based. When demand for block space rises, fee bids rise. The user cannot know in advance which environment they’ll face. A simple USDT transfer on Ethereum costs $5–15+ depending on network congestion, with peak congestion events pushing fees considerably higher. Gas fees fluctuate based on network congestion, typically ranging from $2 to $50 for standard transfers during 2026, and exchanges have responded by setting standardized ERC-20 withdrawal fees of $3.50 to $5 to insulate themselves from the variance.

Tron’s resource model decouples cost from congestion entirely. The network charges fees in a resource model rather than a gas-price auction: senders consume energy and bandwidth which are either burned from TRX or rented from a third party. That fixed-resource design is why TRC20 fees stay flat through volume spikes. As of January 2026, renting 65,000 energy costs about $1.44, and renting 130,000 energy for a fresh-wallet transfer runs about $2.89. Users who freeze TRX in advance pay effectively nothing per transaction.

| Network condition | ERC-20 USDT | TRC-20 USDT |

| Quiet network | $2–5 | $1–3 |

| Normal load | $5–10 | $1–3 |

| Elevated activity | $10–20 | $1–3 |

| Congestion event | $20–50+ | $1–3 |

The implication for retail-scale transactions is decisive. A $20 fee on a $50 deposit consumes 40% of value — no retail business model survives that. Binance’s 2026 withdrawal schedule lists TRC-20 USDT at $1.00, one of the lowest withdrawal fees of any supported network, which is why exchanges defaulted TRC-20 as the retail withdrawal rail.

The predictability matters as much as the absolute level. A platform forecasting monthly settlement costs cannot operate when its fee line item swings 10x based on conditions outside its control. Tron makes financial planning possible. Ethereum makes it a probability distribution.

The tradeoff is decentralization. Tron operates with 27 elected super representatives — closer to a federation than Ethereum’s million-plus validator set. For pure settlement utility this is largely academic; for users who care about protocol-level censorship resistance, it’s a real consideration.

Security and Protocol Compliance

The USDT smart contract has been deployed on Ethereum since 2017 and on Tron since 2019, audited multiple times, and exercised across trillions in cumulative transfer volume. The contract itself isn’t where operational failures occur — the operational layer around it is.

Tether’s blacklist function, callable by the contract owner, has been invoked thousands of times against addresses linked to sanctions, hacks, and fraud. For legitimate operators this is a non-issue in normal operation, but it makes chain analysis screening of inbound deposits a baseline requirement. Major operators typically run Chainalysis, TRM Labs, or Elliptic against deposits before crediting. Tether reports cooperating with law enforcement globally and has frozen billions of dollars in illicit funds since the function was first used.

The most common cause of stuck withdrawals on either network isn’t protocol failure but hot wallet gas exhaustion. Both networks require fees in the native token (ETH or TRX) even when transferring USDT, which means an operator must maintain native-token reserves proportional to withdrawal volume.

| Operational risk | ERC-20 | TRC-20 |

| Smart contract integrity | Negligible risk | Negligible risk |

| Blacklist exposure | Active enforcement | Active enforcement |

| Hot wallet gas exhaustion | Requires ETH reserves | Requires TRX/energy reserves |

| Address format mismatch | User error → permanent loss | User error → permanent loss |

| Major protocol failures (5 yr) | None | None |

Address format errors account for a meaningful share of permanent USDT losses. ERC-20 addresses start with 0x (hex); TRC-20 addresses start with T (Base58). Users routinely copy from one and paste into the other, and some wallet configurations broadcast the mismatch to the wrong network where funds become unrecoverable. The protocol can’t prevent user error — the application layer has to, through explicit network selection at every deposit and withdrawal step.

For high-volume withdrawal pipelines, the practical security posture comes down to three things: chain analysis screening of inbound deposits, sufficient native gas reserves to process outbound transactions without delay, and rigorous address validation at every UI touchpoint. The networks themselves are infrastructure-grade. Ethereum has operated continuously since 2015 with no major protocol failures, and Tron has maintained similar reliability since 2018. Both will continue to carry the bulk of stablecoin settlement volume — the split between them determined by use case, not by fundamental superiority of one over the other.